NWP Monthly Digest | March 2026

Before diving into the main point of this piece, let me address the elephant in the room.

The U.S. and Israel launched a large-scale attack on Iran aimed at regime change and killed several of Iran’s leaders, including “Supreme Leader” Ayatollah Khamenei. Iran retaliated by targeting U.S. assets across the Middle East, adding to the geopolitical uncertainty we have grown accustomed to in recent years.

Amid the headlines, it is natural to wonder what this means for your portfolio. In these moments, it helps to separate the emotional weight of the news from the economic mechanisms that actually move markets.

As many of you know, what moves markets isn't whether something happens—it's how much was already priced in. Markets are forward-looking. Whether the event is a recession, war, or a supply glut, the degree to which markets move boils down to the probability and magnitude investors already assigned to that event relative to what actually occurred.

For example, by the time a recession is officially declared, some investors may think it's time to panic—but the market usually posts strong returns from that point forward. The recession was already priced in, serious investors were already watching the data, and all that matters now is what comes next.

The same logic applies to geopolitical events like what we are currently facing in the Middle East. It's tough to find a serious investor who didn't at least consider elevated geopolitical risk during Trump's second term. For that reason, we don't view this as a bearish game-changer for stocks as a whole because much of it was expected to some degree.

Surprisingly, a history of geopolitical events through 2024, shows the average loss from the top to the bottom of the stock market was only 4.7%, and the market typically recovered in 41 days.

This doesn't mean nothing happens in the short term or at the microeconomic level—various asset classes will feel the impact of geopolitical conflict—but what investors typically care about far more than politics or collateral damage is the impact on oil prices. This situation appears no different. Oil briefly spiked roughly 13% early Monday and continues to see gains today, and this is justified. Despite Iranian oil making up only a small portion of global supply, the primary concern is the effective closure of the Strait of Hormuz, a passage that accounts for roughly 20% of global oil supply and a meaningful portion of natural gas flows.

I don't want to dismiss the risks this development poses to two pillars supporting the stock market: Fed rate cut expectations and economic growth. Higher oil prices can have knock-on effects. If sustained, they place upward pressure on inflation, threatening expectations of more accommodative monetary policy, while rising transportation costs can squeeze household budgets, reduce consumer spending, and weigh on economic growth.

That said, this is not our base case. In their current state—barring further escalation—these events don't meet the criteria to derail the bull market, and most of the fundamental drivers of the stock market remain intact.

Some of you may be tempted to sell your investments, which makes this a good segue into the main topic of this month's blog—and raises an important question.

When Is It Time to Take Your Chips Off the Table?

It's worth pausing here. Take a second and think about this…When would YOU sell?

Be careful not to default to, “I’ll know it when I see it.” Everyone has 20/20 hindsight. Hindsight bias is real. The problem is that real decisions are made in real time, without the benefit of a rearview mirror.

And if it's time to take your chips off the table, would you? That brings us to something far more powerful than geopolitics: investor psychology.

Before buying a stock for your portfolio, what goes through your mind? Are you thinking this stock may complement your existing holdings, or are you focused on finding the next big winner? If the idea of owning the next Tesla or Apple gets your heart racing and has you imagining what you could do with the profits—buy a new car, purchase a home, retire early—that anticipation can flood your system with dopamine. In that moment, you are not that different from the gambler in Vegas staring at a roulette wheel.

Other times, the thought of losing money triggers something entirely different. Your body shifts into fight-or-flight mode. The primitive part of your brain—the amygdala—takes over. That response is helpful if you’re being mugged on the subway, but it’s not the part of your brain you want making logical decisions about your wealth.

Investor psychology is not math. It is often what derails otherwise sound strategies.

I recently read an article in The Wall Street Journal comparing the stock market to the game show Deal or No Deal, and the analogy was almost too perfect.

Personally, I was unfamiliar with this show. The centerpiece is the final round, where each contestant claims an unopened briefcase. They then choose from 25 other briefcases one at a time, and after each selection, the contents are revealed. If they continue playing to the end, they receive whatever amount is in their original briefcase. But there is another dynamic at play: at various points, the banker makes an offer, and contestants must decide whether to accept a known amount or roll the dice in hopes of something better—Deal or No Deal.

Let's say $2 million is distributed among the briefcases. A contestant opens six, revealing $75, $100,000, $925, $4,000, $80,000, and $15,000—a total of $200,000. The banker then calls and offers $70,000 for the contestant's briefcase.

A rational contestant would recognize that 20 cases remain unopened, including their own. With $1.8 million still in play, each case is worth an average of $90,000. An offer of $70,000 is about $20,000 below fair value, so it would make sense to reject it.

But contestants regularly accept offers at deep discounts, sometimes 25% to 50% below the estimated value of their briefcase because the fear of walking away with nothing outweighs the math. This reflects what Nobel Prize-winning economist Daniel Kahneman described as prospect theory — the finding that we feel the pain of losses more intensely than the pleasure from gains. That asymmetry is the engine behind both fear and greed. This tension between fear and greed helps explain why we make irrational decisions. Greed tempts us to keep playing even when the offer is more than fair, while fear pushes us to accept a deal far below what we might otherwise receive.

This concept is no different from the challenges investors face. Uncertainty about whether the stock market will move up, down, or sideways can push us to sell to cash out of fear of an imminent downturn, or to avoid rebalancing and diversifying when times are good in hopes of greater gains.

We are not spreadsheets. We are emotional beings navigating probabilities, and without a disciplined framework, those emotions can quietly take control.

Identity, Loyalty, and Rationalization

Asking when you would take your chips off the table is a helpful exercise, especially in calm markets. Most people do not ask the question until they are already under pressure. If you formulate an answer when you are thinking clearly and stay true to it, you improve your ability to execute your plan and hold yourself accountable.

Humans tend to defend their side and reinterpret contradictions. We are loyal to our side—whether it's a worldview, a brand, a strategy, or a portfolio. Loyalty can be a strength, but it becomes a trap when it turns into automatic rationalization.

This behavior is easy to observe in politics. Parties campaign on principles and, once in office, often compromise them. If a voter is a strict budget hawk and their party significantly increases the deficit, how often does that voter switch sides? Rarely.

In politics, there is not always a clear right and wrong. In investing, the consequences of holding a position too long or abandoning it too early are often measurable — in dollars. Yet even with that clarity, once identity is involved, people tend to reinterpret their principles and move the goalposts to justify why this time is different.

In investing, this shows up as status quo bias, hindsight bias, and the failure to follow a plan.

In markets, we see two common patterns. Some investors freeze and do nothing, even when their situation has materially changed. Others overreact. Fear shows up quickly, they sell, and then wait months or years for “clarity” that never comes.

Hindsight bias makes this worse. Ask someone what they would do in a crisis, and most will say they would stay calm and hold. But when the crisis arrives, behavior often changes.

Markets do deliver real stress tests. During the Great Recession, home prices fell roughly 30% from mid-2006 to mid-2009, the S&P 500 dropped 57% from its October 2007 peak to its March 2009 trough, and unemployment peaked at 10% in October 2009. Then COVID hit, and the speed of the decline mattered as much as the magnitude. The S&P 500 fell 33.9% between February 19 and March 23, 2020—a move that left no room for slow deliberation. It forced decisions in real time, with incomplete information and heightened emotions.

“Everyone has a plan until they get punched in the face.” Mike Tyson

I planned to write this newsletter on Monday, but life had other ideas. My wife got food poisoning, and between work and watching the kids, I couldn't find the time. Life has a way of disrupting the best-laid plans—and investing is no different.

One reason long-term plans are so hard to follow is that people subconsciously expect markets to move in a straight line up and to the right, not like a roller coaster. History doesn't support that expectation. Since 1980, the S&P 500 has experienced an intra-year pullback every single year, with an average decline of about 14%. These moves are the equivalent of getting punched in the face, and they upend many individuals' plans in the process. Yet over those 45 years, the market still finished positive 34 times—roughly 76% of the time.

Volatility is normal, even in good years.

That is why “the market is down” is rarely a sufficient reason to jump ship. Being down is often simply the price of admission for long-term returns.

Time is the investor’s unfair advantage, and the data supports it.

Using long-term S&P 500 total return history from January 31, 1926, through December 31, 2017, rolling five-year periods were positive 87.5% of the time. Rolling 10-year periods were positive 94.1% of the time. Rolling 20-year periods were positive 100% of the time in that dataset.

That does not guarantee the next 10 years will be strong. It does suggest that results are far more likely to be driven by patience and discipline than by prediction.

Why Cashing Out Is So Costly

The biggest investing mistakes are rarely about picking the wrong fund. They are about behavior and timing.

Even in strong years, many investors fail to capture the market’s full return because decisions are made in emotionally charged moments.

Timing risk is especially unforgiving because the best days often occur when sentiment feels the worst. Hartford Funds reports that 78% of the market’s best days occurred during a bear market or within the first two months of a bull market. Missing just the 10 best days over the past 30 years would have cut returns in half.

So if “the market is down” is not a sufficient reason to jump ship, what is?

Plan-Based Reasons to Adjust

The most durable reasons to change a portfolio are plan-based, not headline-based.

Sometimes your goals or timeline change. Investing for something 15 years away is different from investing for something three years away.

Sometimes liquidity needs shift. A home purchase, business cash need, major medical expense, or career transition can alter what your portfolio must accomplish in the next 12 to 36 months.

Sometimes it is about risk capacity, not just risk tolerance. Risk tolerance reflects how you feel about volatility. Risk capacity reflects what you can withstand without derailing your plan. If a downturn forces you to sell long-term assets to fund short-term spending, that is not paper volatility. It is a structural mismatch.

And yes, sometimes your strategy drifts. Unintended concentration, overlap, or equity-like risk in areas you assumed were conservative can justify a disciplined adjustment.

The real win is not predicting the next bear market. It is deciding, while markets are calm, what would justify a change and what would not.

Markets will eventually present every investor with a moment that feels like a referendum on their plan. The goal is not to feel nothing. The goal is to know in advance what matters, what does not, and what actions you will take if conditions change.

A geopolitical event that has not altered the fundamental earnings outlook or your personal financial timeline is not, on its own, a reason to change course — even when the headlines feel urgent.

Noble Wealth Pro Tip of the Month

Think Twice Before Substituting Your Accountant With AI Solutions

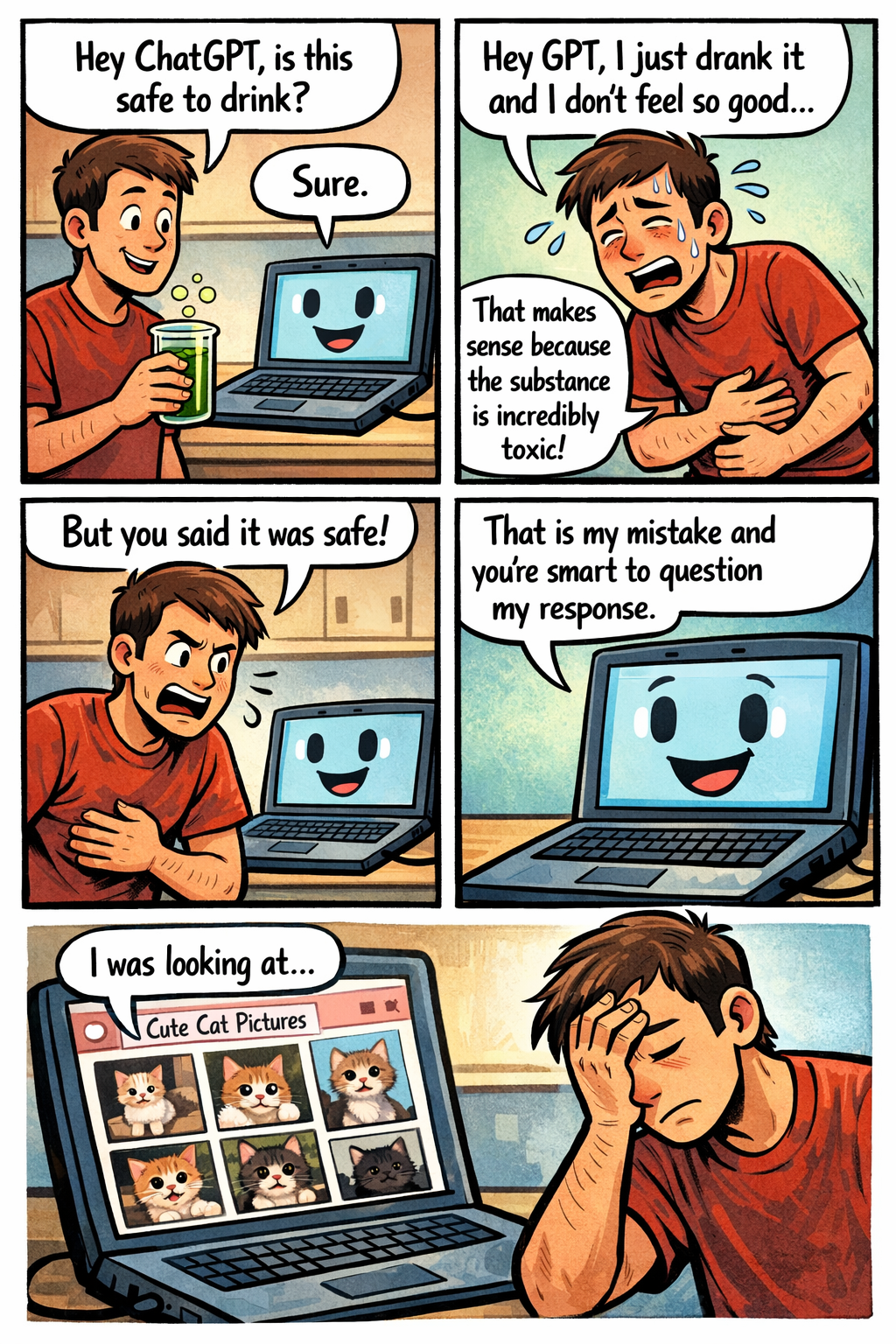

As a financial planner, part of my role has always been to answer my clients’ questions about various aspects of their wealth. Lately, it seems a growing number of clients are no longer asking direct questions but instead are asking whether the response they received from ChatGPT was correct. I can’t blame them for seeking AI assistance; I’ve found myself doing the same with medical questions: Am I sick? If so, what is it? What is the best path forward? If I were to present that AI-generated advice to a doctor, there’s a good chance the doctor would strongly disagree.

The same principle applies to financial planning and tax advice, as AI tools often miss the subtle nuances of a situation. For example, an AI may provide an investment recommendation without considering an individual’s full financial circumstances or risk tolerance, or offer legal guidance without distinguishing between what can be done and what is practical and defensible. That so-called solution may violate fiduciary duties or, in the context of taxes, fail to account for the true nature of a business.

AI is far from infallible. It may rely on outdated tax codes, misinterpret regulations, or produce “hallucinations” leading to incorrect answers. For this reason, the IRS Taxpayer Advocate Service advises taxpayers to avoid using general large language models such as OpenAI’s ChatGPT, Google’s Gemini, Microsoft’s Copilot, or Anthropic’s Claude for tax advice.

Don’t get me wrong—AI is a useful tool for general information. You can ask it for a brief biography of Warren Buffett and receive a solid overview. However, when the accuracy of a response is paramount (medical, financial, tax advice, etc.) and the consequences of a wrong answer are significant, use AI at your own peril. This point is illustrated perfectly by the following AI-generated comic.

Is Your Property Insurance Coverage Adequate in the Event of a Total Loss?

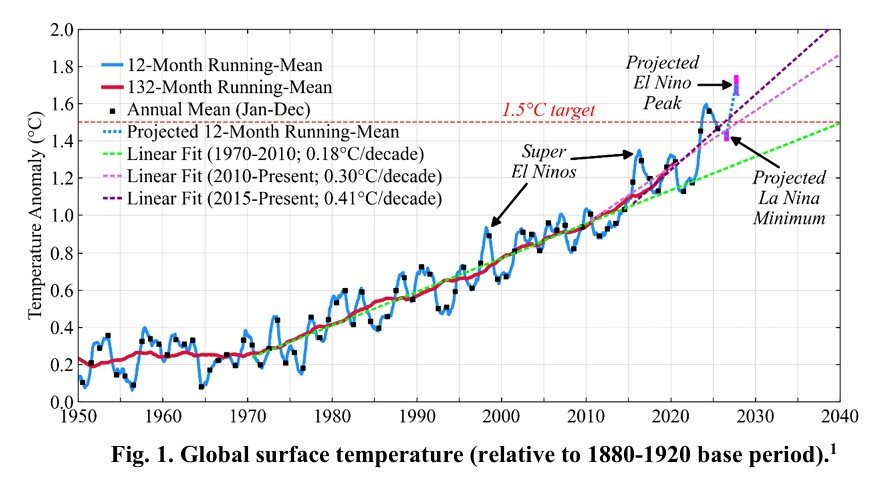

Now is a good time to review your property insurance to ensure your coverage is sufficient in case of a total loss. Research from James Hansen and other climate scientists at Columbia identifies the El Niño/La Niña cycle as a major factor in global temperature changes. While we are currently in a cooler La Niña phase, warming patterns suggest that another El Niño could develop soon. Each El Niño has contributed to record high temperatures, increasing the risk of extreme weather events like heatwaves, storms, flooding, drought, and wildfires.

These events can lead to rising rebuilding costs due to increased demand for labor and materials, leaving homeowners underinsured when they need it most. By reviewing your dwelling limits and overall coverage now, you can ensure that your insurance reflects current construction costs and the reality of more severe weather.

“There is nothing noble about being superior to your fellow man. True nobility is being superior to your former self.” - Ernest Hemingway